If you’ve opened a news app lately, you’d be forgiven for thinking Capital Gains Tax (CGT) is either:

- The root cause of the housing crisis

- A sacred cow that must be protected

- Or a “tax break for the wealthy” long overdue for reform

Depending on which headline you read before coffee.

No wonder people are confused. The Capital Gains Tax debate swings between moral outrage and economic modelling, often without pausing to explain the architecture underneath it all.

So let’s step back from the headlines. No pitchforks. No property evangelism. No tax-shaming. Just a clear look at the three schools of thought, the deeper tax architecture they sit within, and why each camp is convinced it’s right.

Capital Gains Tax Debate Camp One: “The 50% Discount Is a Privilege”

Camp One starts with a simple question:

Why does anyone get half their gain tax-free?

Under today’s rules, if you hold an asset for more than 12 months, half your capital gain disappears for tax purposes. Make a $200,000 profit? Only $100,000 is treated as taxable income.

But here’s the part that often gets overlooked: that $100,000 is added (stacked) on top of your regular income for the year. If you’re already earning well, that additional amount can push you into a higher marginal tax bracket. CGT can therefore feel like a surtax layered onto income tax.

Now for the twist.

Around 71–72% of property investors own just one investment property. Most are genuinely “mum and dad” investors, not multi-property tycoons.

Camp One doesn’t dispute that.

Their argument is different: while most investors own just one property, the largest dollar-value gains tend to be realised by higher-income earners holding higher-value assets. So although participation is broad, the benefit of the 50% discount may not be evenly distributed.

In their view, the discount goes well beyond inflation protection and tilts the system toward those who already had a foothold in asset markets.

Capital Gains Tax Debate Camp Two: “Indexation Was a Better Compass — Tax Only Real Gains”

Camp Two responds with a history lesson.

Australia introduced Capital Gains Tax in 1985. From then until 21 September 1999, the system relied on indexation, meaning your asset’s cost base was adjusted for inflation (CPI) before calculating the gain.

In 1999, the 50% CGT discount was introduced as part of broader tax reforms. For assets held at that time, taxpayers were given a choice:

- Continue using indexation (frozen at September 1999 values), or

- Switch to the new 50% discount method.

After that date, indexation was no longer available for new gains, and the 50% discount became the standard rule for individuals holding assets longer than 12 months.

Here’s why Camp Two still prefers the older approach.

Take a simple example from a higher-inflation era. If you bought a property in 1987 for $300,000 and sold it in 2007 for $900,000, the nominal gain would be $600,000. Under today’s 50% discount, only $300,000 of that gain would be taxable.

Under indexation, however, the original 1987 cost base would be adjusted for inflation, particularly through the late 80s and early 90s when CPI was much higher than it is today. If inflation lifted the cost base to, say, $500,000, the taxable gain would instead be $400,000, representing only the increase above inflation.

In other words, indexation attempts to strip out price-level movement before tax is applied, whereas the 50% discount simply halves the gain regardless of how much of it reflects real growth.

When inflation is low and asset prices surge, the 50% discount can look more generous. But in inflationary periods, indexation can appear more economically precise.

That’s the core of Camp Two’s argument. Less dramatic than “half your gain vanishes”, and more aligned with the principle of taxing real, not nominal, growth.

Capital Gains Tax Debate Camp Three: “CGT Should Be Its Own Tax. Separate, Predictable, and Transparent”

Camp Three says the real anomaly isn’t who gets a discount, it’s that CGT is grafted onto the existing income tax system at all.

Right now, your capital gain gets added to your assessable income. That can catapult you into a much higher bracket, especially when your regular income is already substantial, meaning a once-off gain can be taxed at top marginal rates. To some, that feels less like taxing profit and more like penalising timing.

This camp looks abroad for inspiration.

In the UK, capital gains are taxed under a separate CGT regime with their own rates and reporting rules. For residential property, gains are generally taxed at:

- 18% for basic-rate taxpayers

- 24% for higher and additional-rate taxpayers

Importantly, property gains must be reported and paid within 60 days of completion, separate from the annual income tax return.

There is also an annual CGT allowance (currently modest, but still distinct), and the gain itself doesn’t “stack” into income in quite the same way Australia’s system does.

The UK model isn’t necessarily perfect, but it demonstrates a structural alternative:

- Separate CGT rates

- Separate reporting timelines

- Clear distinction between earned income and capital gains

To Camp Three, reform in Australia could look like:

- A distinct CGT regime with its own rate schedule

- A prompt reporting and payment deadline (similar to the UK’s 60-day rule)

- Thresholds or allowances to protect smaller investors

In other words, treat capital gains as a stand-alone economic event, not just another line item folded into income tax.

Housing’s Star Turn. But It’s Not the Whole Show!

Whenever CGT enters the spotlight, housing follows like a stage-hand adjusting the lighting.

Critics argue the 50% discount (paired with negative gearing) fuels investor demand and inflates prices. Defenders argue investor participation supports rental supply.

The truth? Housing markets are deeply complex. Construction costs, zoning laws, immigration settings, policy-driven demand incentives (like first-home buyer grants and new-build concessions), finance conditions and supply constraints all interact.

Blaming CGT alone for housing affordability is like blaming the seatbelt for the car crash.

The Revenue Reality Check (And Why It Feels Lopsided)

Here’s the part that rarely makes the front page.

Australia’s tax system leans heavily on individuals. Personal income tax makes up around half of total federal government revenue. That’s before you factor in GST, fuel excise, stamp duties at state level, land tax, council rates etc, the list most households quietly fund every year.

We are, structurally, a system funded primarily by workers.

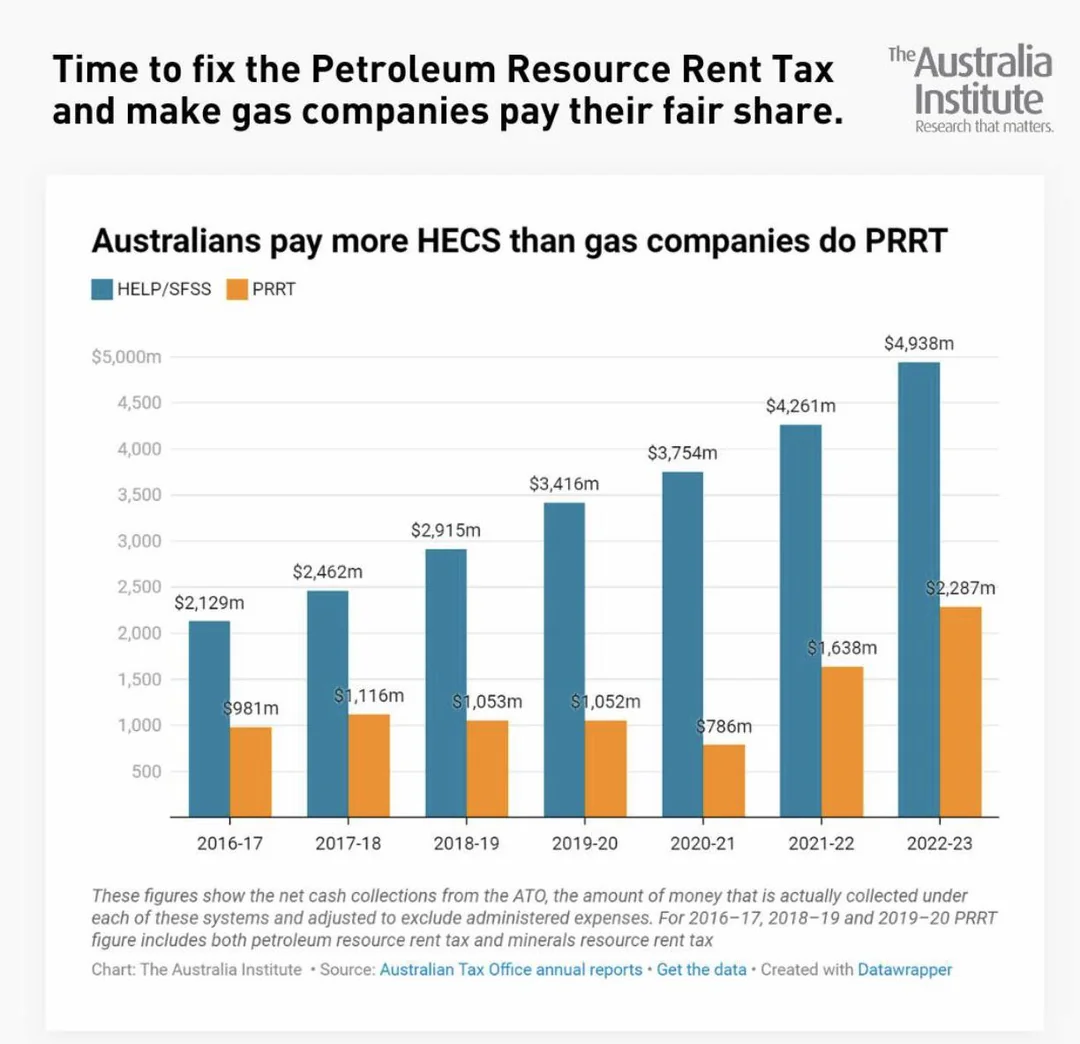

Now for a comparison that puts things in perspective.

In 2023–24, Australians repaying HECS/HELP student debt contributed more than four times as much revenue as the Petroleum Resource Rent Tax (PRRT) raised from oil and gas companies. Roughly $5 billion from student debt repayments versus about $1 billion from PRRT in the same year.

That doesn’t mean resources aren’t taxed at all. But it does highlight something uncomfortable:

Income earned by individuals, and even student loan repayments, currently contribute more reliably to federal revenue than taxes on extracting non-renewable natural resources.

And yet, when tax reform discussions heat up, the spotlight often swings to capital gains, superannuation balances, negative gearing or bracket creep, not to whether we’re capturing full economic value from resources that belong to the public.

Which brings us back to the bigger question:

The debate about CGT isn’t just a technical tax issue, it’s nested inside a much larger conversation about who pays what in our tax system, and whether we’re getting a fair return on assets that belong to all Australians.

If reform is about fairness, it’s worth asking whether we’re looking in the right place.

The Takeaway. A Story with Less Noise, More Nuance

Here’s the honest summary:

- Camp One sees the 50% discount as a structural privilege that tends to benefit higher-income taxpayers and produce uneven outcomes.

- Camp Two reminds us that a more neutral design, like indexation, can ensure tax is levied against real, inflation-adjusted gains.

- Camp Three wants CGT treated as its own tax event with clear rules, possibly separate rates and reporting deadlines, a model that might reduce the “income stacking” effect that pushes people into higher brackets.

And all this happens in a system where:

- Individuals pay the lion’s share of revenue.

- Natural resource wealth isn’t fully captured for public benefit.

- The loudest headlines often miss the core economic questions.

Debates about CGT aren’t just about fairness. They’re about tax design, efficiency, who shoulders the burden, and how we balance incentives with revenue needs.

If you come away from the debate still a bit confused, that’s because it is complicated. Any serious reform should reflect that complexity, not turn Aussie taxpayers against each other while the bigger tax questions go untouched.

Want to make managing your capital gains easier? TaxTank helps you track, calculate, and plan your CGT with confidence, so you can focus on making smart investment decisions without the stress. Get started with TaxTank today.