Tax season in Australia can often be a daunting and overwhelming period for everyday Australians. Navigating through the intricate web of tax regulations and requirements can lead to various pitfalls that might cost you both time and money.

However, armed with the right knowledge and expert advice, you can ensure a smooth and error-free tax time. In this comprehensive guide, we’ll delve into essential strategies to help you avoid common tax mistakes and make the most of your tax return experience.

Here are some key strategies and insights to help you navigate tax season successfully:

1. Understanding Your Tax Obligations and Deadlines

Navigating the Australian tax landscape starts with a clear understanding of your tax obligations. In Australia, the financial year runs from July 1st to June 30th, and individuals are required to lodge their tax returns by October 31st each year. This return should include income from various sources, such as employment, investments, and rental properties. Staying informed about these obligations and deadlines ensures that you fulfil your tax responsibilities and can plan your finances effectively.

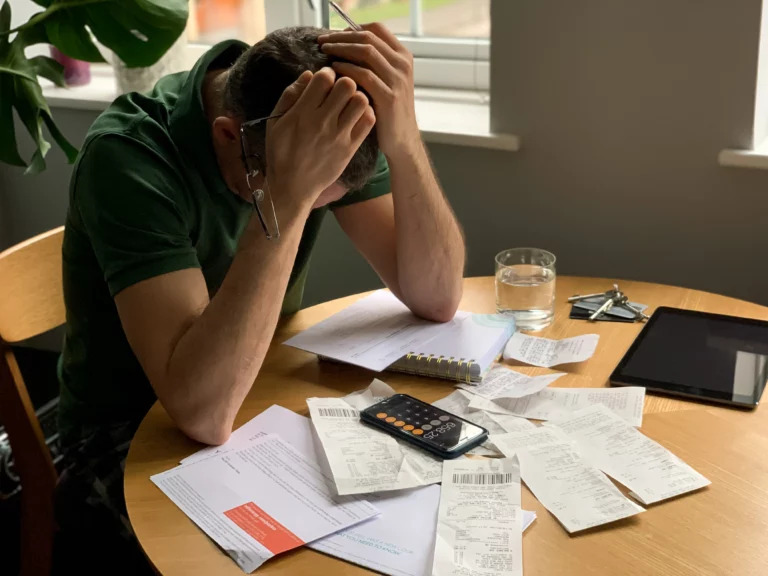

2. Organised Record-Keeping To Avoid Common Tax Mistakes

Maintaining well-organised records is a cornerstone of effective tax management. Keep all relevant documents, such as receipts, invoices, and financial statements, neatly categorised and easily accessible. Utilise digital tools and tax software to streamline the process. Expert advice: Regularly reconcile your financial records to identify discrepancies. Using a tax software like TaxTank, lets you connect live bank feeds to reconcile income and expenses throughout the year.

3. Accurate Income Reporting

Accurately reporting your income is essential to avoid unnecessary common tax mistakes and further scrutiny from the ATO. Ensure that all sources of income, including wages, investments, and rental income, are accurately reported in your tax return. Insider tip: Cross-reference your bank transactions with your reported income to ensure consistency.

4. Claiming Eligible Deductions

Maximising deductions can significantly reduce your taxable income. Familiarise yourself with eligible deductions relevant to your situation, such as work-related expenses, charitable donations, and rental property expenses. Keep supporting documentation handy to substantiate your claims. Pro tip: The Australian Taxation Office (ATO) provides a comprehensive list of allowable deductions.

5. Understanding Capital Gains Tax (CGT)

If you’ve sold assets such as property, shares or crypto during the year, you may be liable for Capital Gains Tax. Understanding how CGT works is crucial to accurately calculate and report your capital gains. Seek expert advice if you’re unsure about CGT implications. Expert insight: CGT discounts may apply if you’ve held the asset for over a year.

6. Avoiding Last-Minute Rush

Procrastination often leads to mistakes and oversights. Avoid the last-minute rush by starting the tax preparation process well in advance. This allows you ample time to gather necessary documents, review your returns, and seek professional assistance if needed. Pro tip: Using tax software can help you manage your time and effort throughout the year instead of trying to do everything at the last minute.

7. Double-Check Details Before Submission

If you’re self lodging your tax return take a moment to double-check all the details in your tax return before hitting the submit button. Ensure that you’ve accurately entered all figures, deductions, and personal information. A simple typographical error could lead to unnecessary delays and potential discrepancies. Expert insight: Reviewing your return multiple times can catch some of the most common tax mistakes.

FAQs (Frequently Asked Questions)

Is it mandatory to hire a tax professional?

Engaging a tax professional is not mandatory, but if you have complex financial situations, a tax professional can help you navigate intricate tax laws and optimise your returns.

What are some common red flags that could trigger an ATO audit?

The ATO may initiate an audit if they detect inconsistencies in your reported income, excessive claims for deductions, or suspicious offshore transactions. Maintaining accurate records and transparent reporting can help you avoid audits.

Can I claim deductions for home office expenses?

Yes, you can claim deductions for home office expenses if you meet certain criteria. The ATO allows deductions for work-related expenses incurred while working from home.

What is the penalty for late lodgement of tax returns?

The penalty for late lodgement of tax returns can vary depending on your circumstances. It’s generally advisable to submit your returns on time to avoid potential penalties, which can accrue over time.

How can I stay updated on changes to tax regulations?

To stay updated on changes to tax regulations, regularly visit the ATO’s official website and subscribe to their newsletters. Additionally, tax professionals often stay informed about changes and can provide guidance.

Final thoughts

Tax time in Australia doesn’t have to be a stressful ordeal. By understanding your obligations, staying organised, and seeking expert advice when needed, you can avoid common tax mistakes and navigate the process with confidence.

Remember, accurate reporting and proactive preparation are key to a successful tax season. Why not try TaxTank for a free 14-day trial and start feeling more confident about the upcoming tax season. It’ll transform the way you think about and manage tax so you don’t have to stress about ATO crackdowns!